Posted on Tuesday, May 5, 2020

Posted on Tuesday, May 5, 2020As the nation responded to the COVID-19 pandemic, bars and restaurants across the nation were shut down by local or state edict with no known re-opening date in sight. Other restaurants scaled way back to skeletal crews, providing take-out orders only. However, restaurants were not the only businesses that shuttered operations. As more and more states and local communities went under “Stay Home,” “Safer at Home,” or “Shelter in Place” orders, a variety of businesses, from small shops to entire office buildings, became devoid of customary operations with their usual occupants furloughed or on WFH (work from home) status.

Beware of the (no) vacancy provision! Almost every commercial property policy has some variation of a vacancy or unoccupancy provision. In the standard ISO property policy form, the vacancy provision is found in the policy’s “Loss Conditions” section. In one insurer’s commercial property policy, the vacancy provision is found in a section titled “Limitations.” Yet another property insurer’s policy has a “Vacancy – Unoccupancy” provision under the “Other Conditions” section. While most commercial property policies only use the term “vacant,” some policies distinguish between the terms “vacant” and “unoccupied.” State amendatory endorsements tend to use the term “unoccupied.”

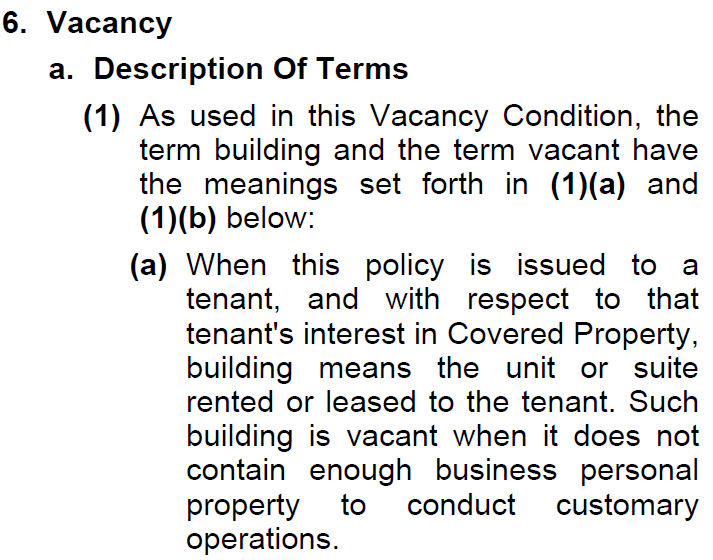

What do these vacancy provisions say? In each of these commercial property policies, if the insured building is “vacant” for more than 60 days before a loss occurs, there is no coverage if the loss is caused by: vandalism, sprinkler leakage (unless the insured protected the system against freezing), building glass breakage, water damage, theft, or attempted theft. For all other covered losses, the insurer will reduce the insured’s recovery under the policy by 15% if the vacancy provision applies. The ISO property policy describes “vacant” as follows:

Consider the following three claim examples from my state, California, as interpreted under the standard ISO “Vacancy” provision above. California Governor Newsom issued the first statewide stay home order on March 19, 2020. The executive order directed all residents to stay home indefinitely. Exemptions exist for operations deemed “essential.” Restaurants are “essential” for purposes of take-out and delivery, but not otherwise.

Example 1:

Policy issued to tenant who rents from building owner: A popular bar in my neighborhood shut down immediately. In addition to a sign on the door stating that it was closed until further notice due to the statewide COVID-19 order, it also posted a sign on the door stating that it had no liquor or cash on the premises, presumably to discourage theft.

If the bar has an ISO standard commercial property policy and is a tenant in the building, under section (1)(a) (quoted above), would the removal of the liquor from the premises mean that the bar was “vacant”? If so, and operations are shut down past May 19 (60 days after the statewide order), the bar stands to lose valuable coverage.

Example 2:

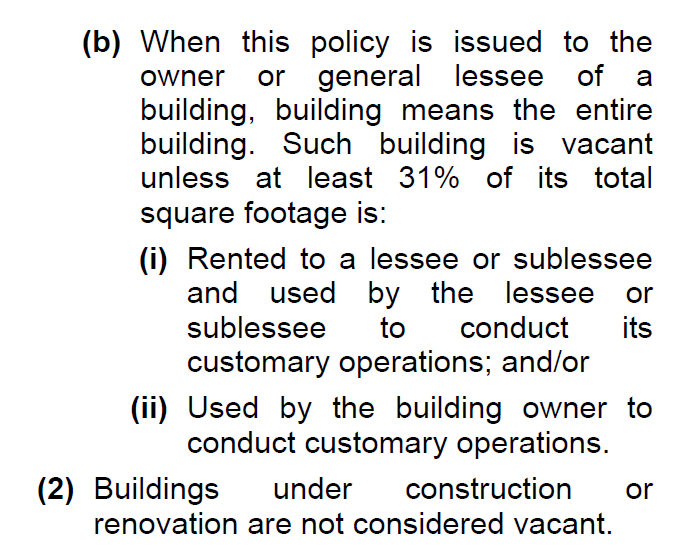

Policy issued to owner who rents to tenants: A mall (i.e., a building containing several shops and restaurants) is closed for business. Note that, under part (1)(b)(i), if the policyholder is the owner of the building and the building is used by its lessees and/or sublessees, at least 31% of the building’s total square footage must be rented to a lessee or sublessee, and 31% of the square footage must also be “used by the lessee or sublessee to conduct its customary operations.”

Can the building owner satisfy this requirement right now? Under the policy, will the building be considered “vacant” if the shops or restaurants that occupy at least 31% of the mall’s total square footage cannot conduct customary operations for 60 consecutive days?

Example 3:

Policy is issued to building owner who occupies the building: A high-end restaurant (not geared for take-out) owns and operates its own restaurant building. Under the California statewide order, the restaurant is considered non-essential (except when offering take-out and delivery), so it shut down its operations. Note that under section (1)(b)(ii), if the building is owner-occupied, at least 31% of the building’s total square footage must be “used by the building owner to conduct customary operations.” After 60 days, this restaurant, if its commercial property policy contains the ISO “Vacancy” provision, will be deemed “vacant” and will lose valuable coverage.

Some state amendatory endorsements go even further and allow the insurer to cancel coverage if the building is unoccupied for 60 consecutive days. For example, the Illinois amendatory endorsement (ISO form IL 02 84 12 05) allows for cancellation of a commercial property policy in effect for more than 60 days (and only if the policy covers real property other than residential property occupied by four families or less) if the building has been unoccupied 60 or more consecutive days (with exceptions for seasonal unoccupancy and buildings under repair, construction or reconstruction, if the building is properly secured against unauthorized entry). The North Dakota amendatory endorsement (ISO form IL 02 34 09 17) allows for cancellation of a property policy in effect for more than 90 days if at least 65% of the rental units in the building are unoccupied, or if the building has been unoccupied for 60 or more consecutive days (except buildings with seasonal occupancy or those in the actual course of construction or repair, and the building is properly secured against unauthorized entry).

If your business has been shut down for an extended period of time, we advise that you check your property policy for a no vacancy or unoccupancy provision. You can contact your broker and request a waiver of this provision or an extension of time from your insurance carrier. We have it on good authority from a national broker, however, that property insurers have not been receptive to making any changes to their policies that would expose them to additional COVID-19 exposure, including in the area of vacancy and occupancy. Therefore, policyholders should consider hiring extra security or taking other measures to protect their property from loss.

For more information, contact Melanie A. McDonald at mam@sdvlaw.com.

Click on this link to view the article in pdf format