Posted on Thursday, October 18, 2018

Posted on Thursday, October 18, 2018I. Introduction

Recent amendments to Florida’s Statute of Repose1 have resulted in concerns as to the scope of risk Florida homebuilders face as a result, and the availability of insurance coverage for such exposures. Previously, the statute provided for a strict, yet straightforward 10-year limitation for latent construction defect claims. Under that language, issues arose when suits were filed near expiration of the statute, because parties seeking to defend claims were given little time to effectively assert related claims. The amendment to the statute serves to lengthen the statute of repose to 11 years for certain cross-claims, compulsory counterclaims, and third-party claims, and in limited circumstances, potentially even longer. Most policies in the Florida marketplace serve to limit coverage under the products-completed operations hazard (“PCO”) to 10 years, and thus, in very limited circumstances, an insured contractor may be exposed to third-party claims under the revised statute. It is important to note, however, that coverage under most CGL policies is occurrence-based, meaning that the policy is triggered by property damage that occurs during the policy period, and therefore, any subsequent claims permitted under the amended statute will necessarily relate to the original property damage that occurred during the 10-year period, and thus, would be covered under the standard 10-year PCO extension. This paper will analyze the anticipated effect of the amendments upon coverage under a 10-year PCO extension.

II. Understanding the Relationship Between the Statute of Repose and Insurance Coverage

A. Amendment to Florida Statute 95.11(3)(c)

On March 23, 2018, the Governor approved House Bill 875 which became effective on July 1, 2018. This bill amended Florida Statute 95.11, which governs statutes of repose for construction defect claims and previously provided for a strict 10-year statute of repose. Pertinently, the amendment includes the following addition: “However, counterclaims, cross-claims, and third-party claims that arise out of the conduct, transaction, or occurrence set out or attempted to be set out in a pleading may be commenced up to 1 year after the pleading to which such claims relate is served, even if such claims would otherwise be time-barred.” This language seeks to extend the time to file claims for latent construction defects for up to an additional year, or 11 years from the date of completion of the project. The new limitations period applies to any actions that commence on or after July 1, 2018.

B. Effect of Amendment on Products-Completed Operations Coverage

Currently, in the Florida market, most policies provide products-completed operations coverage for 10 years, or the statute of repose, whichever is less. This begs the question of whether the amendment to the statute has created any uninsured exposure outside of the scope of the PCO hazard.

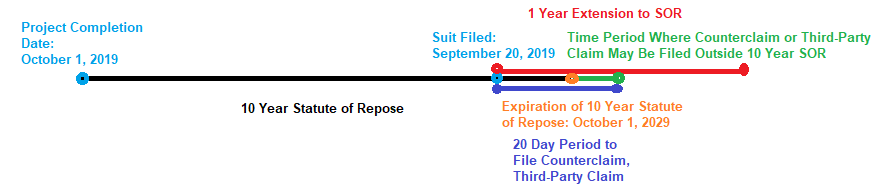

To evaluate the potential for uninsured exposure, we start with the fact that the set of circumstances in which this extended limitation period may come into play at all is limited. First, in order for the repose period to be expanded under the revised statute, a defect claim would need to be asserted in the 10th year after project completion, on the eve of the expiration of the limitations period. Florida’s Rules of Civil Procedure require a party to assert all counterclaims, cross-claims, and third-party claims within 20 days of the filing of the pleading triggering the claim.2 Thus, taking into account any potential extensions of the time period to respond, if the statute of repose expires within that time frame, a compulsory counterclaim, a cross-claim, or third-party claim that arises from the same conduct will not be barred pursuant to the amended language. In other words, in the 11th year, either a compulsory counterclaim would need to be asserted against the party bringing the original action, a cross-claim asserted by one defendant against another, or a new party would be joined in the action by way of a third-party claim. In the latter scenario, where another party is joined in the 11th year, the language of the statute arguably allows that party an additional year to assert claims, resulting in potential exposure up to 12 years after project completion. This may not have been the legislative intent for the period to extend anywhere beyond 11 years,3 however, the revised language permits such a result.

As seen in the following illustrated hypothetical where suit is filed September 20, 2019, assuming the 20-day period to file a counterclaim, cross-claim or third-party claim is not extended, there is only a brief period of time (highlighted in green) in which claims may fall outside the original 10-year statute of repose.

Even more limited are the situations where the extended repose period under revised Florida Statute Sec. 95.11(c) could result in a potentially uninsured exposure outside of the extended comp-ops period. Coverage under most CGL policies is occurrence-based, meaning that the policy is triggered by bodily injury or property damage that occurs during the policy period, including the 10-year PCO extension period.

As such, the original lawsuit will in most cases be brought by the owner of the property within the 10-year statute of repose. The statute further requires that any subsequent claims by or amongst the parties must arise out of the same occurrence set out in the original pleading. Thus, by the statute’s plain terms, any additional claims will in most circumstances relate to the original occurrence and allege the same property damage that occurred during the policy period and was the subject of the initial pleading. Therefore, most subsequent claims allowed by the amended statute (regardless of when they are asserted) will relate to the property damage that occurred during the policy period, and thus, be covered by the 10-year PCO extension.

Further, under general pleading principles, compulsory counterclaims and cross-claims filed by or against an insured, who is already party to the action, will necessarily relate back to the property damage that is the subject of the original filing, which occurred during the policy period, and therefore covered. This is because if the insured is part of the action from the beginning, any cross-claims or compulsory counterclaims filed will relate back to the initiation of suit, therefore falling with the 10-year statute of repose and be covered under standard PCO language. Moreover, although it does not appear that Florida courts have addressed the issue, the majority rule is that the duty to defend does not include the obligation to prosecute counterclaims.4 Thus, to the extent the insured may seek to bring a counterclaim, it may not be covered regardless of the potential expiration of the PCO period. Therefore, if we assume a 10-year PCO extension that begins to run upon project completion, the only situation that could potentially result in exposure outside of the 10-year PCO period is where an insured is first brought into the defect action by way of a third-party claim asserted in the 11th or 12th year after project completion, which relates back to the property damage asserted in the original filing, but is considered a separate occurrence for purposes of coverage.

Although the circumstances are temporally and procedurally limited, the resulting consequences to an insured may be significant where a third-party claim is asserted, and coverage ultimately denied as a result of the 10-year PCO extension period having expired.

C. The Marketplace

A review of carrier offerings shows that a majority of the PCO endorsements provide completed operations coverage for “10 years, or the applicable statute of repose, whichever is less.” In fact, most PCO extensions commercially available in the Florida marketplace are effectively limited to 10 years, and coverage for extension periods greater than 10 years generally not offered. This is likely the result of a majority of the project-specific insurance markets being London syndicate insurers or reinsured through London, which limits PCO extensions by treaty to 10 years.

D. Recommendations

To ensure the revised legislation does not negatively impact coverage, it is recommended that any extended PCO endorsement utilized going forward not be restricted to a specific number of years alone (i.e., 10 years), but instead state that the PCO Hazard is extended to the applicable statute of repose. In addition, endorsements that specifically state “10 years, or the applicable statute of repose, whichever is less. . .” should also be avoided to ensure there are no resulting uninsured exposures. Alternatively, language reading “10 years, or the applicable statute of repose, whichever is greater. . .” would be acceptable.

III. Conclusion

Although the amendments to the statute have yet to be interpreted by courts, the recommended best practice is to be proactive and review PCO extensions on a going forward basis to identify language that explicitly limits the coverage afforded to 10 years. The potential uninsured exposure a Florida homebuilder may face, while low in probability, can often be curtailed by modifying the PCO extension period to apply through the applicable statute of repose.

For more information contact Rich Brown at rwb@sdvlaw.com (203.287.2115) or Grace Hebbel at gvh@sdvlaw.com (203.287.2128).

Click here for the updated copy of the Statutes of Limitations and Repose for Construction-Related Claims 50 State Survey.

______________________________________________________________________________________

1 See Fla. Stat. Ann. § 95.11 (West), titled Limitations other than for the recovery of real property.

2 See Fla. R. Civ. Pro. 1.40 (a)(1); Fla. R. Civ. Pro. 1.180(a).

3 The House of Representatives Final Bill Analysis suggests that the limit is intended to be no more than one additional year, stating that the statute is amended “to extend the time to file counterclaims, cross-claims, or third-party claims up to one year beyond the current statutes of limitations or repose in an action based on the design, planning, or construction of an improvement to real property. This bill allows such claims to be filed up to one year after the filing of the triggering pleading in actions based on the design, planning, or construction of an improvement to real property, even if those claims would otherwise be time-barred.” (emphasis added.)

4 See, e.g., Spada v. Unigard Ins. Co., 80 Fed. Appx. 27, 29 (9th Cir. 2003) (duty to defend does not extend to the insured’s affirmative claims); Vansteen Marine Supply, Inc. v. Twin City Fire Ins. Co., 2008 WL 599850 (Tex. App. Mar. 6, 2008) (insurer’s duty to defend did not obligate it to pay for policyholder’s purely offensive counterclaims); James 3 Corp. v. Truck Ins. Exchange, 91 Cal. App. 4th 1093, 1104 (Cal. Ct. App. 2001); Goldberg v. Am. Home Assur. Co., 80 A.D.2d 409, 410 (N.Y. App. Div. 1981).

Click on this link to view the article in pdf format